- All Post

- Brandenton

- CAM

- Clearwater

- Commercial Real Estate Agents

- Commercial Real Estate Education

- CRE News

- East Tampa

- Florida Commercial Real Estate

- Foreclosures

- Hillsborough County

- Historical Sales Info

- Hotel-Resort

- Industrial/Flex

- Industry Spotlight

- Lakeland

- Largo

- Location

- Manatee County

- Multifamily

- National & Global Commercial Real Estate

- Office For Lease

- Office News

- Office Property For Sale

- Office Space

- Pasco County

- Pinellas County

- Pinellas Park

- Plant City

- Press

- Property for Rent

- Property for Sale

- Retail For Sale

- Retail News

- Retail Space For Rent

- Retail Vacant Commercial Real Estate Tampa

- Rocky Point

- Section 1031 Exchange

- St. Petersburg

- Tampa

- Tampa Bay Business News and Commentary

- Tampa Bay Commercial Property Rental

- Tampa Bay Restaurants

- Tampa Commercial Real Estate News and Commentary

- Transportation

- Uncategorized

- Video

- Westshore

- Westshoree

- Zip Code

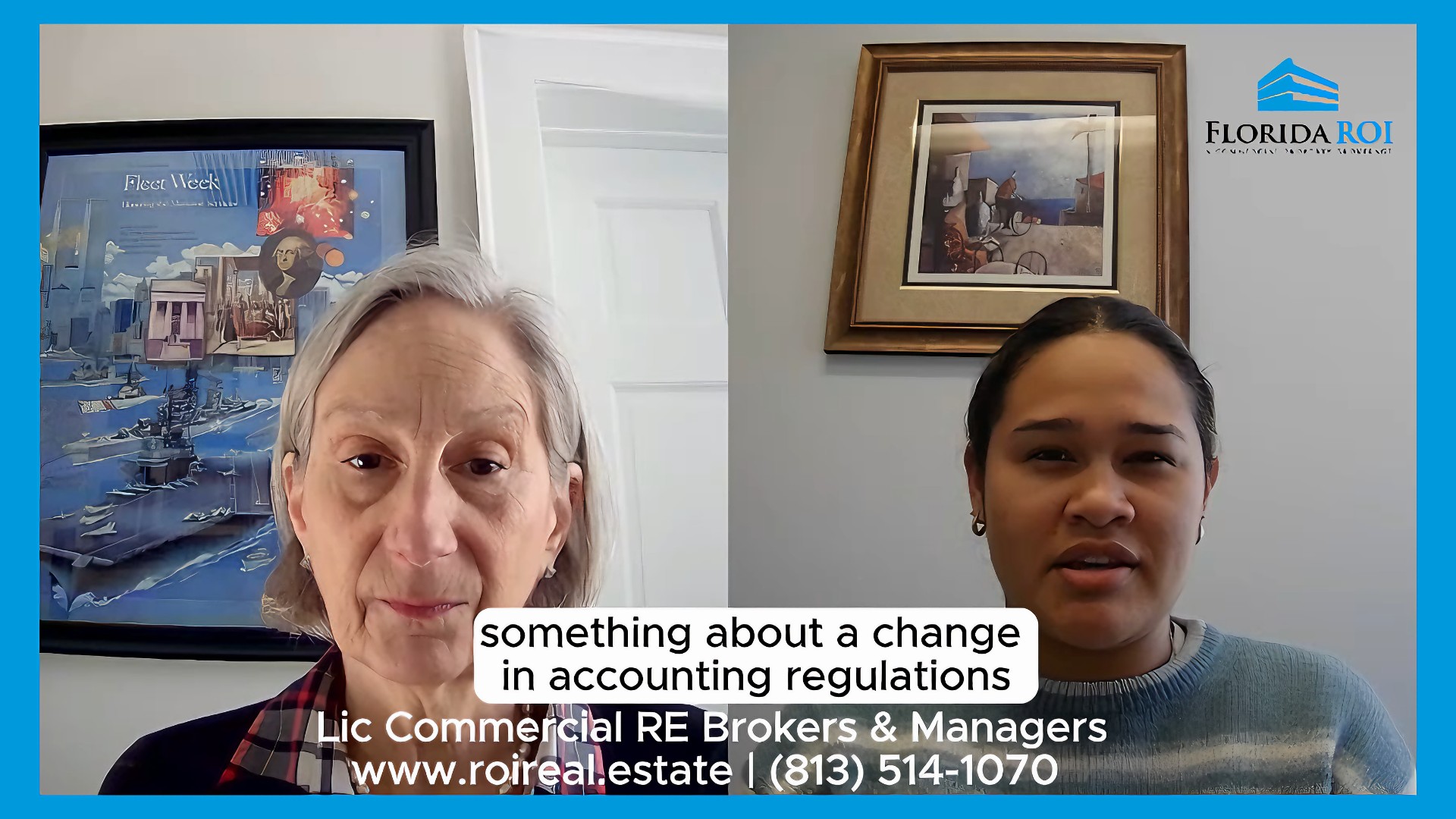

[Transcript from video] Bryana (00:02.602) Hi, I’m Brianna. I’m an intern here at Florida Investment Real Estate and I’m a junior at the University of Tampa. And today we’ll be talking to another one of our fellow agents, Ms. Jill Coulter. Jill Coulter (00:15.436) Hi Brianna, how are you doing today? Bryana (00:17.642)…

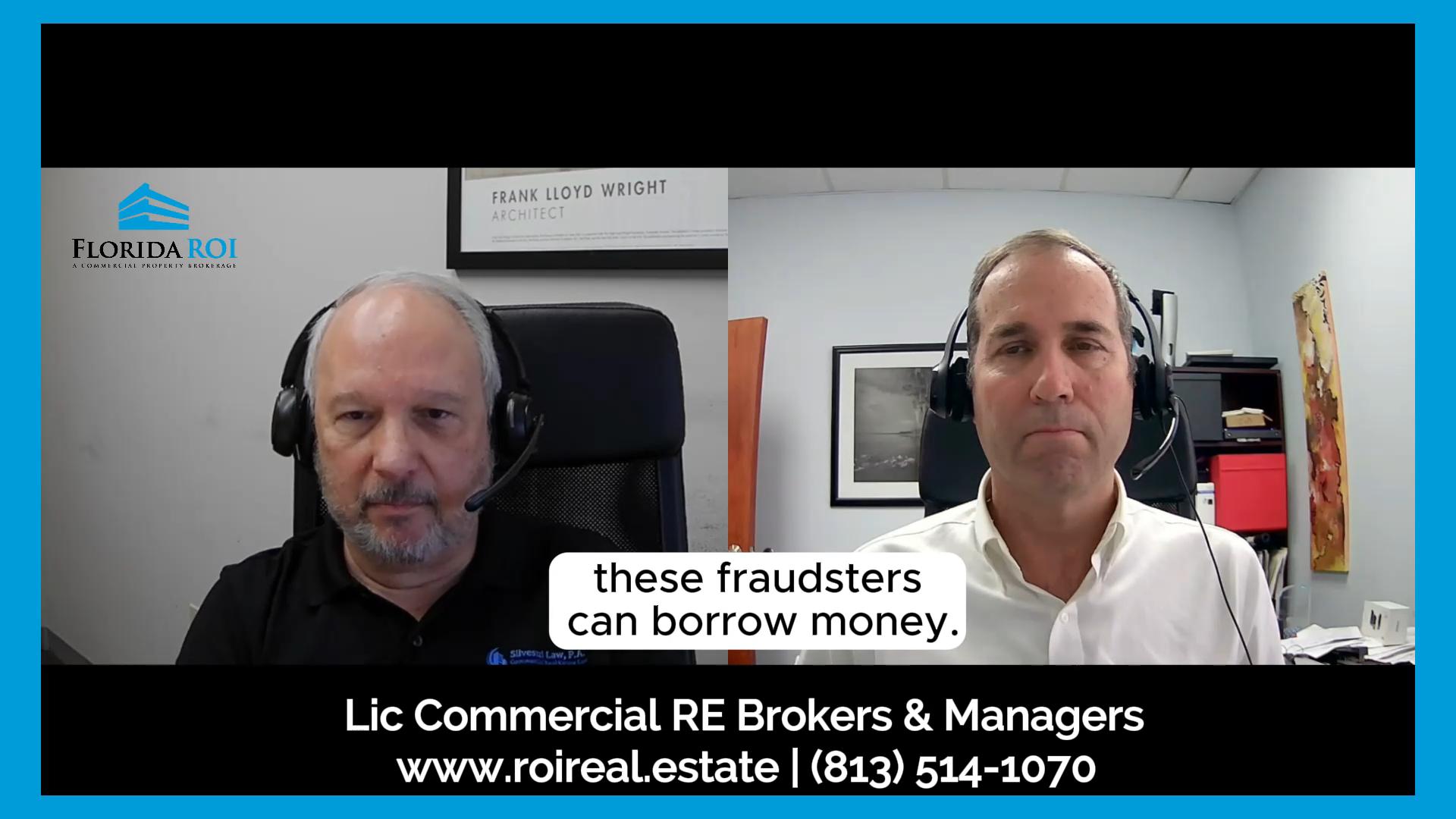

[Transcript from video] Eric Hello, I am Eric Odum, the Broker for Florida ROI Commercial Property Brokerage here in Tampa, Florida and wanted to take just a minute to introduce one of our attorneys that we use on a regular basis, Larry Silvestri. Larry, correct me if I’m wrong, I think you have…

Hello, I’m Eric Odom Broker for Florida ROI Commercial Property. I just wanted to shoot a quick video to address an issue that has come up with a number of clients. It has to do with estate taxes, and there are potential changes coming to these estate tax laws and commercial real estate…

Introduction For commercial real estate investors navigating the dynamic landscape of the Tampa Bay Area, understanding the concept of “grandfathering” in zoning regulations is paramount. From its legal framework to its practical applications, this article serves as an indispensable resource for investors seeking clarity in their real estate ventures. Understanding Its Relevance In…